According to S&P Capital IQ, distressed debt ballooned by 15% in the month of February alone, totaling a whopping US$327B, up 265% from a year ago.

The number of S&P rated US companies with distressed debt rose 9% in February, up 128% from a year ago.

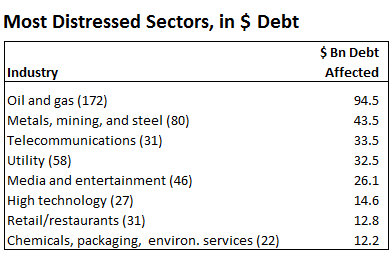

This is an indication that risks are spreading across the broad spectrum of the US economy. Here is a list of the most distressed sectors:

As the oil and gas sector is the more distressed industry, I expect there will be more provision for credit losses once the banks report the Q1 2016 financials. Just last week, JP Morgan increased its provision for credit losses by another 60% (US$500M).

Once the oil and gas sector starts to unravel, it will implode the credit and financial derivative markets, and we could have a major financial crisis at hand.

Besides the oil and gas sector, the subprime students loans (US$1.3T) and car loans (US$1.0T) are raising the prospect of a major default by borrowers, students who cannot find a job, and car owners who over leveraged their personal finances.

Ignoring the U3 and U6 data, if we take into account of every citizen who is of employable age, the unemployment rate in the US could be more than 20%.

The coming months could be telling on the stock market.